The following piece is a white paper written by Chris Walton and Takeoff Technologies that was first published via LinkedIn on September 15th, 2020. It is now republished for Omni Talk with Takeoff’s permission.

Any time Takeoff puts out new research on how retailers should think about the online grocery business, I eat it up (pun intended). It gives me a chance to sit back, to collect my thoughts, and to rechallenge my thinking about everything happening with the industry.

Because, boy oh boy, have things been a- changing.

Covid-19 rushed onto the scene like a bat of hell. E-grocery adoption has accelerated at a rapid pace, grocery retailers across the board have seen banner sales results, and yet it is hard to know what to make of it all. Is it just a case of grocers being in the right place at the right time—i.e. people still needing food, not being able to leave their homes, and so what the heck else are they supposed to do?

Or, is there something more for us to understand in terms of how everything is playing out?

We can talk of subscription programs with “+” signs attached to the end of them, third-party delivery services signing up retail partners faster than Liz Taylor goes through husbands, but, without looking hard at the data, we run the risk of it all being window dressing for short-term success that will only confuse things down the line.

All of which is why I again found Takeoff’s latest research paper in its ongoing series on e-groceries so compelling. Sure, the coronavirus has made it feel like e-groceries are finally set to ramp up, but how and why we all feel that way deserves a closer look.

Three important data points from Takeoff’s latest research, for instance, may already indicate the path to success that the best-of-the-best grocers will ultimately choose.

#1 — Grocery customers expect to get their groceries delivered same-day

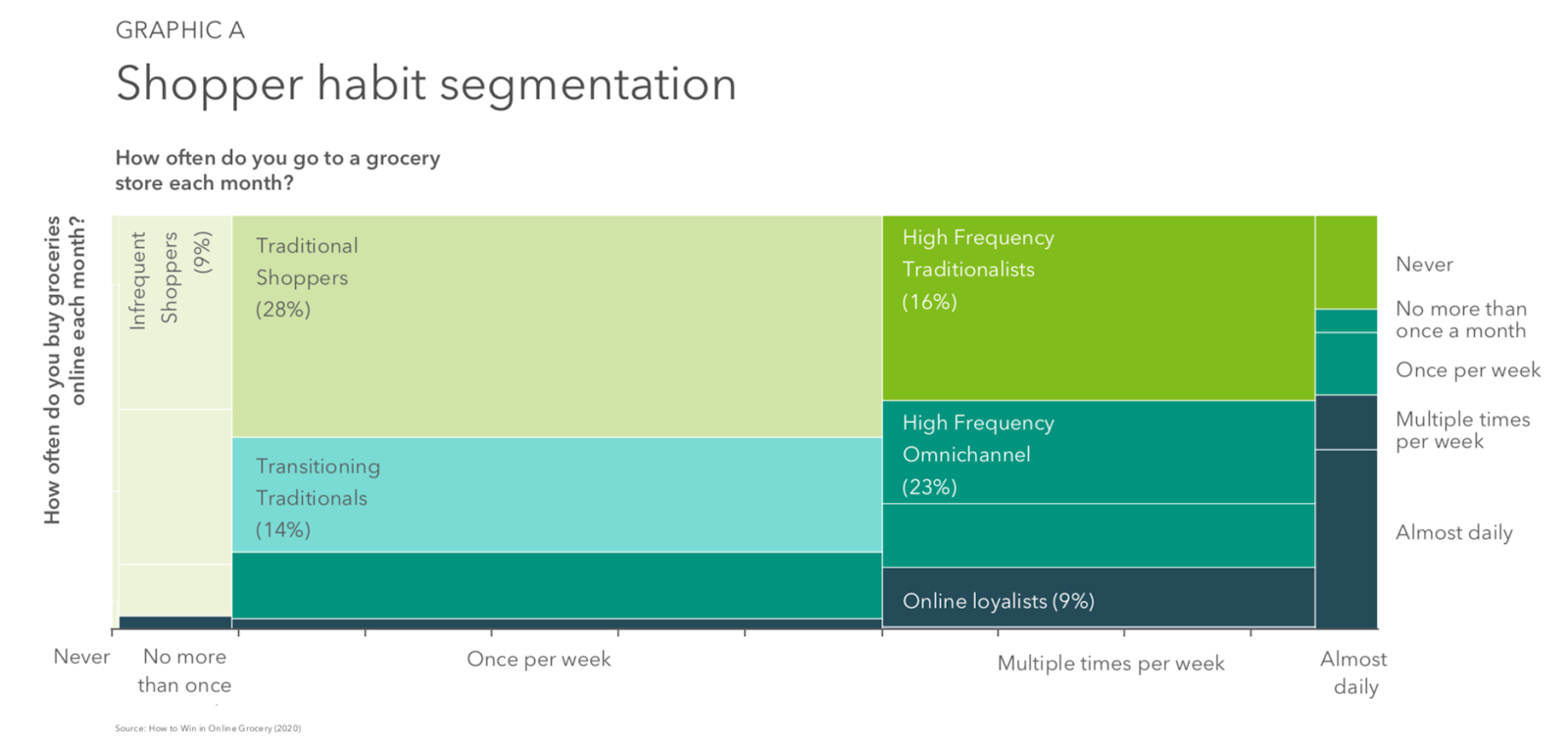

Takeoff’s latest research, conducted in partnership with Timothy M. Laseter, Professor of Practice at the Darden Business School at the University of Virginia, surveyed over 1,000 consumers just prior to the pandemic and broke them into six various cohorts (see below):

Essentially, each of the cohorts identifies the varying degrees that people shop in-store vs. online. For example, “Traditional Shoppers,” the largest category of respondents (28%), never shop online, while “High Frequency Omnichannel” shoppers (23%) tend to shop both online and in-store multiple times per week .

The classifications, while cool, are not the important point here, though. The important factor is that, regardless of the classification, the psychological expectations across the cohorts are nearly identical when it comes to delivery timing. Grocery consumers expect their groceries to be available same-day or better and have negative feelings about any processes that take longer than that.

Remember, this data is pre-pandemic, too. So, it is easy to see why things like Instacart, curbside pickup, and BOPIS have taken off. They all solve the literal same or “same-day” problem, i.e. that people expect to get their groceries quickly.

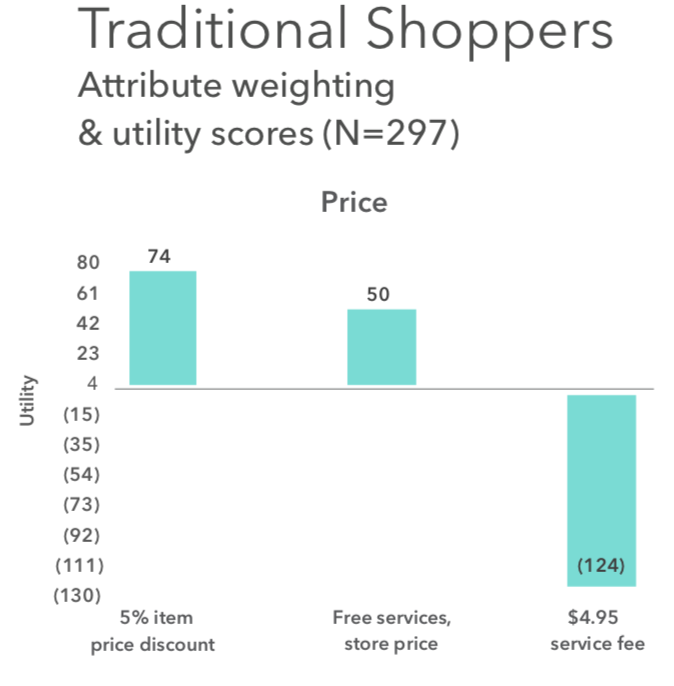

#2 — Price is and likely will always be a key factor in grocery

Delivery timing isn’t the only part of the story, either.

Price is and will always be a factor. When some retailers are running up almost 25% year-over-year, it isn’t because they have done something that much better than the next guy. It is because they are sitting at the nexus of forced habit change.

Let me explain what I mean.

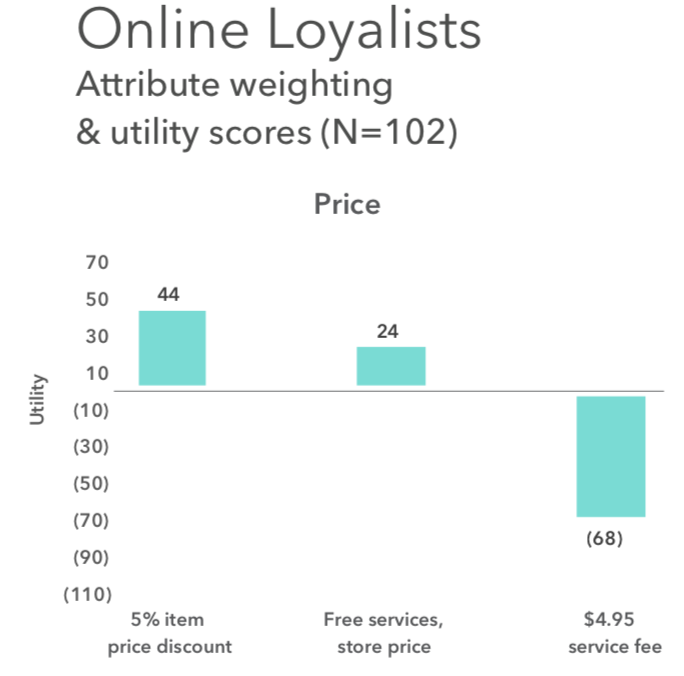

Universally, the survey data shows that people do not want to pay service fees for delivery (see below):

This aversion to fees is an important part of the pandemic puzzle because it helps to put programs like curbside pickup or buy online, pickup in-store in the proper context. In essence, these programs all give people the opportunity to try e-groceries and to get things the same-day without ever having to pay a price premium.

This is fundamentally why companies that were prepared to offer same-day curbside and BOPIS services across their fleets have been thriving. These services play to zeitgeist of the moment and, most fundamentally, underlying consumer expectations.

Or said another way, when the average American household only makes $60,000 per year, third-party delivery service fees may not be an option for everyone.

#3 — Grocery shopping will never be an all or nothing (i.e. stores vs. digital) equation

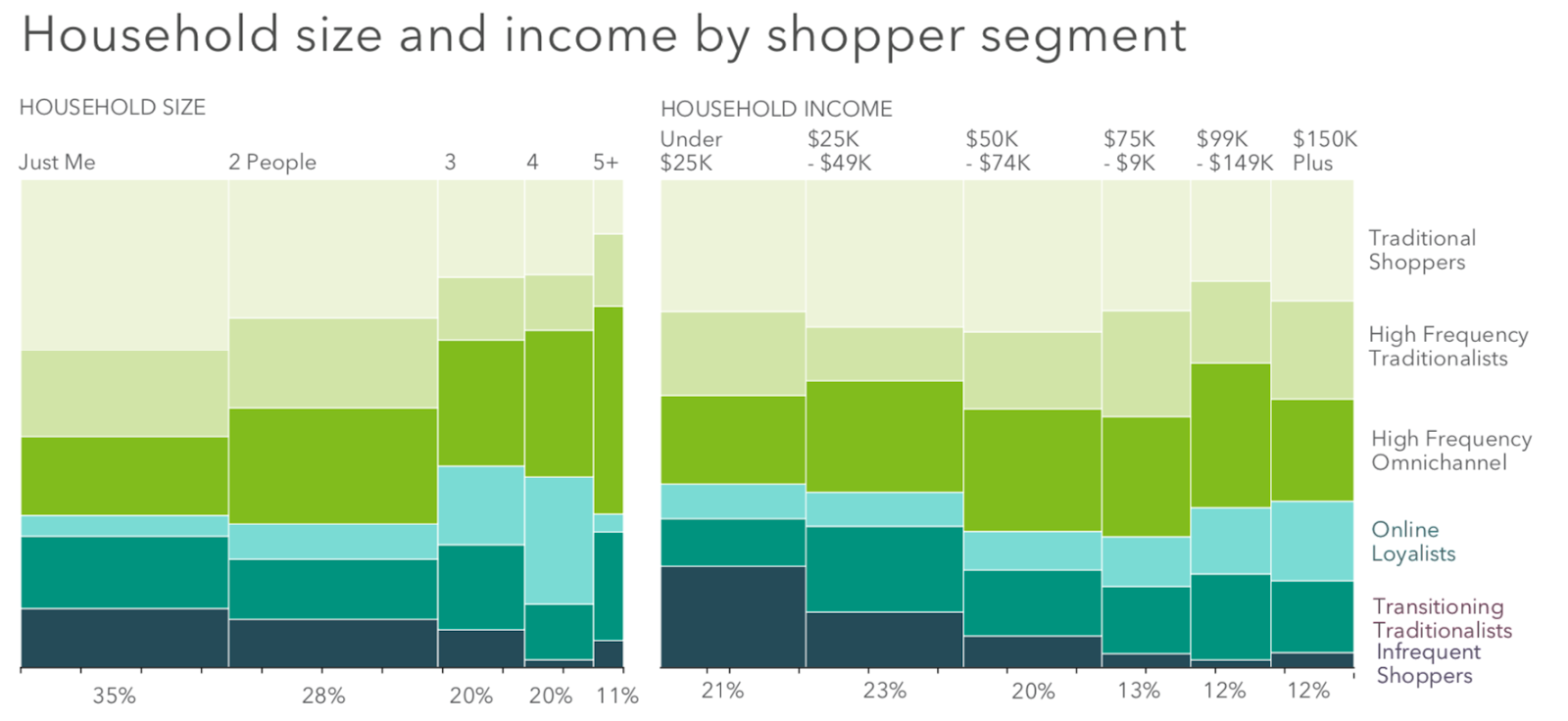

Two final parts of the research hit me like a kiss at the end of a wet fist. One has to do with household size, while the other has to do with evidence already available overseas. Both prove that stores and digital combined will likely always be key elements of the average shopper’s routine in some way, shape, or form.

According to the research, household size is a better predictor of whether one shops online than household income (see below). Households of 4 or 5+ shoppers exhibit the highest rates of online shopping, at almost 68% and 71% respectively.

Why would this be, you might ask?

Because people are busy. The more people living in a household, the less time people likely have to go to the store and also the more likely people are to run out of what I call “onesie” or “twosie” items. Even store-going traditionalists, according to the survey, as they start to test the waters of online grocery, report supplementing their weekly shopping trips with online orders in this same manner.

But, while people need digital, people also still need stores.

Even the majority of the most loyal of online shoppers (aka the “Online Loyalists,” who make up 9% of the surveyed population) report still going into grocery stores weekly. Look overseas, where e-groceries are far more advanced than here in the U.S., and rates of penetration in some places (like the U.K., for example), already peaked years ago at just 49%.

Taken together, stores and digital both matter and must coexist within an ecosystem, and not as the walled gardens of which they are operationally so often conceived.

Implications

Time, price, and flexibility. Those are the key three words after reading Takeoff’s latest report. They capture it all. The inertia of the moment, but also the pragmatism of how one should approach the accelerating e-grocery adoption curve.

When one looks at everything posited above, the case for large centralized and automated warehouse facilities goes right out the window. Sure, they can help retailers to pick and pack goods more efficiently, but can they really meet the delivery timing expectations of the American consumer day in and day out?

Probably not.

Same goes for third-party services. They might seem like a smart stop gap when all the world is burning down amid a pandemic, but over time, they too are relatively more pricey for both consumers and for retailers.

Localized automated fulfillment, on the other hand, brings with it proximity to customers for delivery, efficiency for picking and packing, and leverages an inventory asset base inside of physical stores that consumers, too, will always want in some fashion. All of which brings a higher return on invested capital.

Hindsight may be 20/20, but so too is foresight when it comes to putting this pandemic-filled 2020 year, 2020, into the right perspective and predicting where the future of grocery is headed.

The future is local, automated, and operating right out of stores that already exist.

To download a PDF of this article, click here

Omni Talk® is the retail blog for retailers, written by retailers. Chris Walton and Anne Mezzenga founded Omni Talk® in 2017 and have quickly turned it into one of the fastest growing blogs in retail.

Omni Talk® is the retail blog for retailers, written by retailers. Chris Walton and Anne Mezzenga founded Omni Talk® in 2017 and have quickly turned it into one of the fastest growing blogs in retail.